Visit our archives for more gold & silver articles.

We have always put emphasis on the need to diversify while putting together your portfolio. Of various kinds of diversification, one is particularly important at the very beginning, when you decide to commit yourself to the precious metals market. This is the ability to divide your capital into three separate parts, each managed in a different way, and to stick with this structure even when the market is getting hot.

We are of the opinion that such a division:

- Limits your risk,

- Provides significant upside potential and exposure to the great bull market in silver and gold,

- Takes into account key major factors that could come into play in the following years like a collapse of financial system, and lack thereof.

So what is exactly our suggested portfolio structure? Please, take a look at the table below.

A short description of this structure:

- Insurance - this is your protection against the large financial crisis that is very likely to be seen in the next decade. You may have read somewhere that even those who hate gold and silver should still own some "just in case." This insurance part of your portfolio is kept in precious metals. It’s essential that it be held in physical bullion; geographically diversified if possible at all times -even if you think that gold and silver are likely to decline.

- Investment – this is the part of your portfolio that like the insurance part is kept invested for the long term. Unlike the insurance part of the portfolio, you can temporarily limit the exposure by hedging or selling your holdings before highly probable and significant declines (like the 2008 one).

- Trading capital – this is the part of your portfolio that you use for trading i.e. for betting on short-term rallies and/or declines in gold, silver and/or mining stocks.

While the general idea of dividing your portfolio between long-term and speculative capital (the latter is only the money you can afford to lose) is not a particularly new one, the inclusion of the insurance part in the portfolio may make it more robust to financial blow-ups. We will now focus on that – gold and silver as insurance against severe financial turmoil.

Gold may be perceived as insurance if you believe that, because of psychological reasons, it appeals to investors as a wealth-preservation vehicle. In case of financial turmoil they turn to precious metals, the increased demand causes an increase in the price and gold and silver deliver on their promise to provide an alternative to government bonds.

There is also another dimension to it: in the past gold and silver were used as money. As a matter of fact, gold had been indirectly used as money up to 1971 when U.S. president Richard Nixon officially announced that the U.S. government would cease to adhere to its promise to redeem the greenback in gold. Since that moment money has been only paper and a promise of the government to accept payments in it.

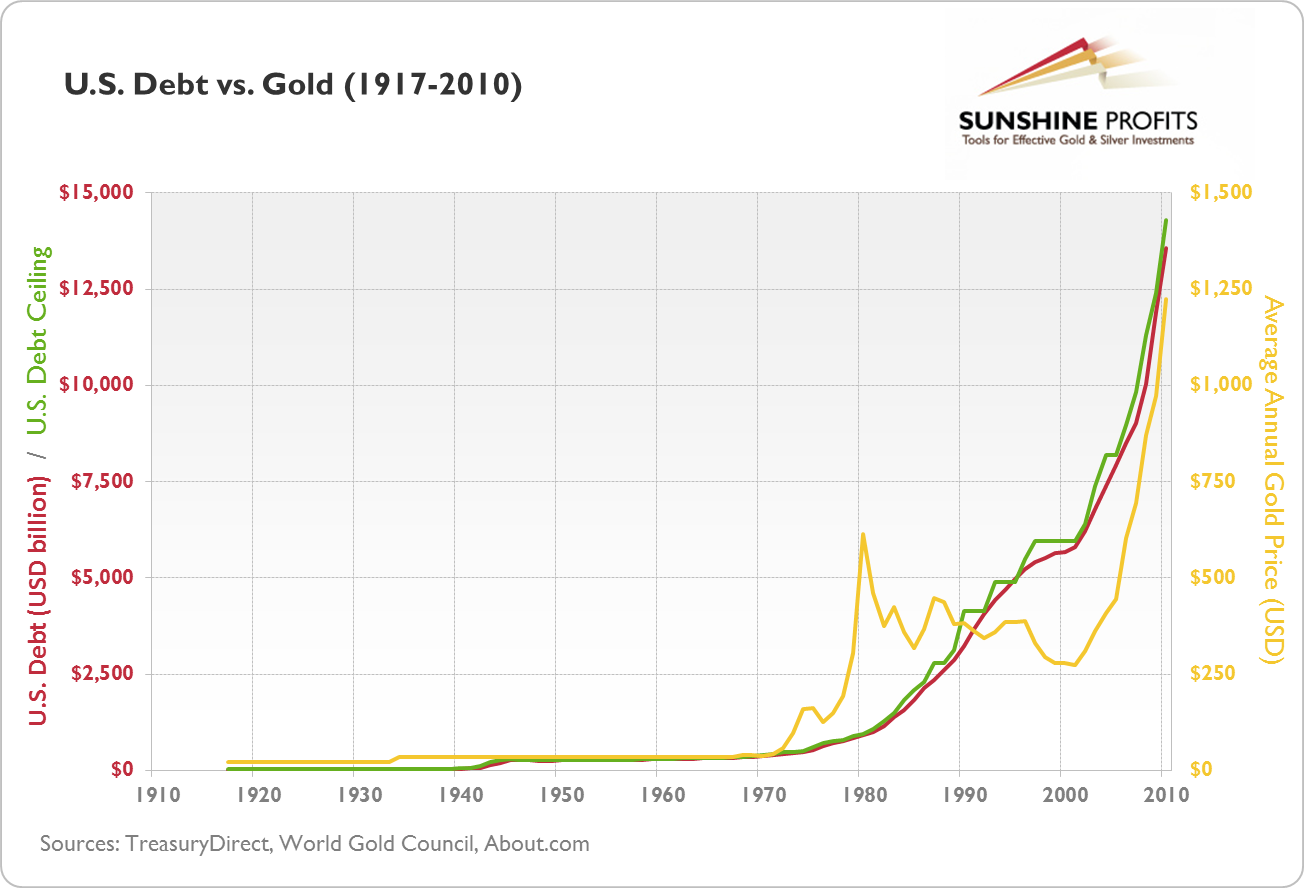

Some investors fear that excessive deficits as seen in the U.S. will result in money being printed on a large scale (which actually is already the case: open-ended QE) or even in the implosion of the dollar. The bigger the deficits, the more likely such a scenario seems. This is shown on the chart below.

It seems that since 2000 increases in the U.S. debt have been accompanied by increases in the price of gold. This might reflect investors’ fear that the U.S. government will eventually default and their belief that gold may be a safe haven in case of such a development.

The abovementioned points may lead to the conclusion that gold may in fact skyrocket if things get out of hand in the U.S. or in the European Union. The main problem here is that nobody knows when (if at all) the paper currencies will begin to visibly deteriorate or disappear completely. Precisely because of that, we suggest holding on to gold and silver at all times with a part of your portfolio.

We call this part of your portfolio “Insurance,” because by holding on to gold and silver even during corrections you accept small losses in hope of enormous gains should serious economic turmoil materialize. Economic crises have the inherent quality of catching most investors off-guard. We don’t want you to be among them.

This is, however, not all there is to gold as insurance. Namely, the idea described above only makes sense if the insurance part of your portfolio is put into physical gold, NOT into any kinds of gold futures, options, ETFs, ETNs or CFDs. If the scenario you are insured against (a financial crisis far more severe than the one that started in 2008) occurs, gold derivatives will most likely be rendered worthless or trading rules will change in a way which will prevent you from fully enjoying your profits. What is more, your counterparties could default on their obligations leaving you with nothing at all.

Even though such a course of events seems unlikely, it is still a possibility you need to consider. Particularly if you keep in mind that in the past serious appreciation of metals led to enormous increases in margin requirements for futures contracts. This was the case for palladium in 2000.

In 2000 palladium appreciated from the level of $443 to the level of $956 boasting a stunning rate of return of 115.8%. During that time, however, the New York Mercantile Exchange raised margin requirements for palladium futures contracts in a series of steps which brought the margins as high as to $168,750 for a $72,000 contract. That meant that just to maintain your position open and reap the profits, you had to make a deposit exceeding the size of your position by 133.1%(!) At one point, the Tokyo Commodities Exchange even ceased trading palladium futures and demanded all positions in futures be liquidated.

If this case is anything to go by, exponential growth in the price of gold or silver (possibly 100% in one year) during the third stage of the bull market could result in hikes in margin requirements or in trading restrictions on the part of commodity exchanges. This alone could render paper gold, futures, options and other financial instruments not backed with physical gold worthless or at least suppress their value. And if you realize that your counterparty could simply go bankrupt or default on their obligations, it becomes clear that from the insurance point of view physical gold and silver (or physically backed funds) are the only way to go.

To add an additional layer of insurance to your holdings, you should also diversify your physical holdings geographically. This is an appropriate way to preserve your investments if capital controls are introduced or governments begin to confiscate precious metals.

You can read more on the topic of how to divide your investment capital in our essay on gold and silver portfolio structuring. You will also be able to find an exhaustive list of methods to invest in gold and silver in our guide on how to buy gold and silver.

In order to make sure that you won’t miss any of our free essays, we strongly suggest that you sign up for our gold & silver investment mailing list. Sign up today and you’ll also receive 7 days of access to our premium updates, market alerts, premium charts and tools. You’ll also receive 12 best practice e-mails as a starting bonus. It will take less than a minute and if you don't like it, you can easily unsubscribe anytime.

Thank you.

Sincerely,

Przemyslaw Radomski, CFA