Briefly: in our opinion, full (300% of the regular position size) speculative short positions in junior mining stocks are justified from the risk/reward point of view at the moment of publishing this Alert.

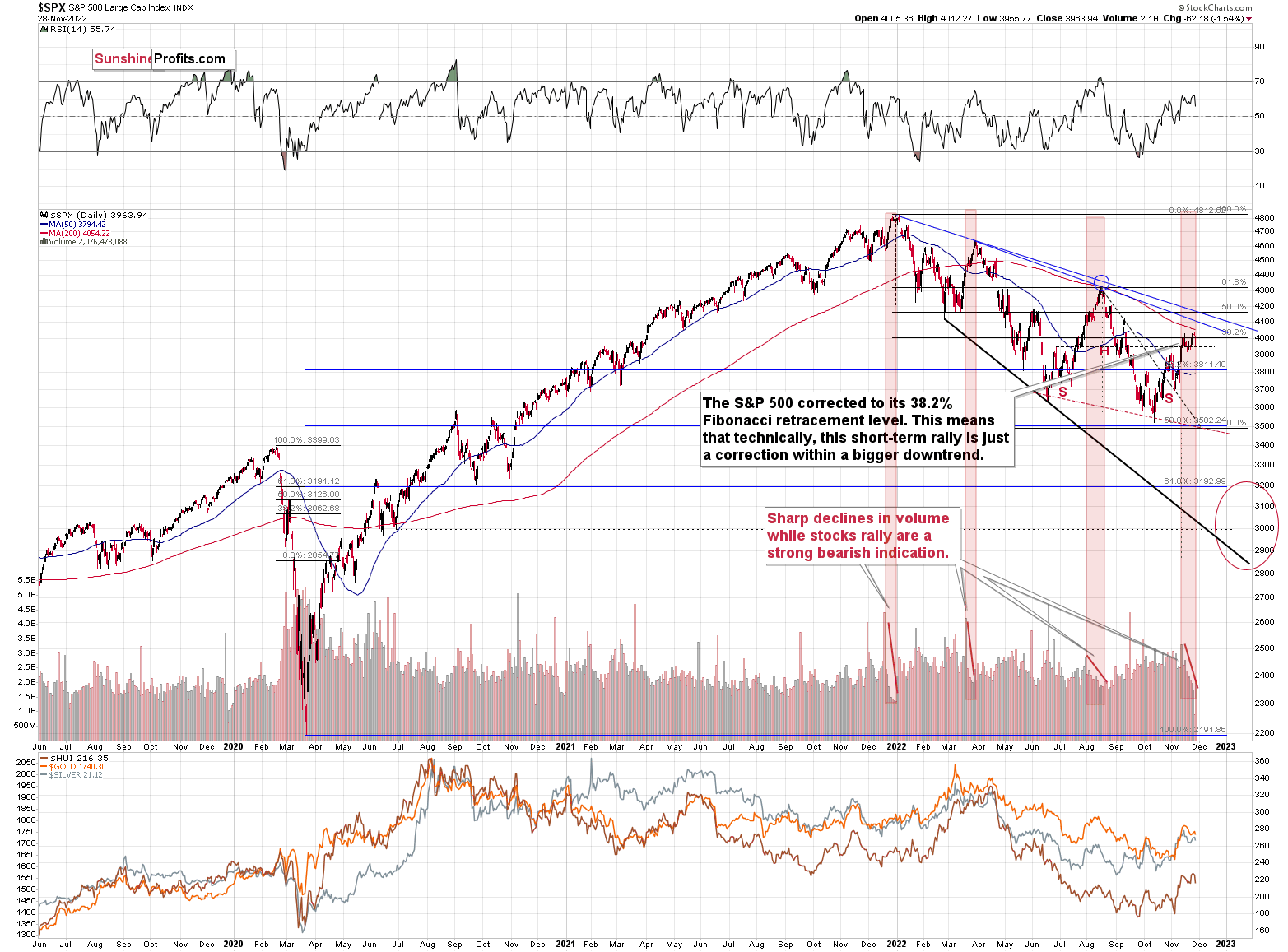

In yesterday’s analysis, I wrote that the stock market was likely to invalidate its recent upswing above its 38.2% Fibonacci retracement level, and that’s exactly what happened.

I wrote the following:

We just saw a small attempt to break above the 38.2% Fibonacci retracement, and I doubt that this breakout will be confirmed. The “why” behind it is currently the most interesting analogy that we see on this market.

Please take a look at the areas marked with red rectangles. In all those cases, the S&P 500 index rallied on big volume at first, and then the volume declined over the course of a few weeks. And as that happened, the price approached its top.

All three previous important tops that we saw this year were accompanied by this indication.

We also see it right now.

Even more interestingly, the volume levels that have just been seen are similar to the ones that accompanied previous tops.

Consequently, it seems that the end of the rally is near. This is likely to have very bearish implications for junior mining stocks.

Stocks declined and ended the day below the above-mentioned 38.2% Fibonacci retracement and the 4,000 level, which has profoundly bearish implications for the following weeks.

Indeed, junior miners’ prices fell substantially during yesterday’s trading.

When viewed broadly, a drop of more than 5% is not that significant, but it is, in my opinion, not so huge yet. Silver’s price was down more than gold’s (1.42% vs. 0.78%), but junior miners declined the most. Even more than senior miners – the GDX ETF was down by 4.01%.

No wonder – junior miners’ prices have the strongest link with the performance of the general stock market, and as the rallying stocks uplifted juniors in the previous weeks, now they are likely to drag juniors lower. Likely much lower.

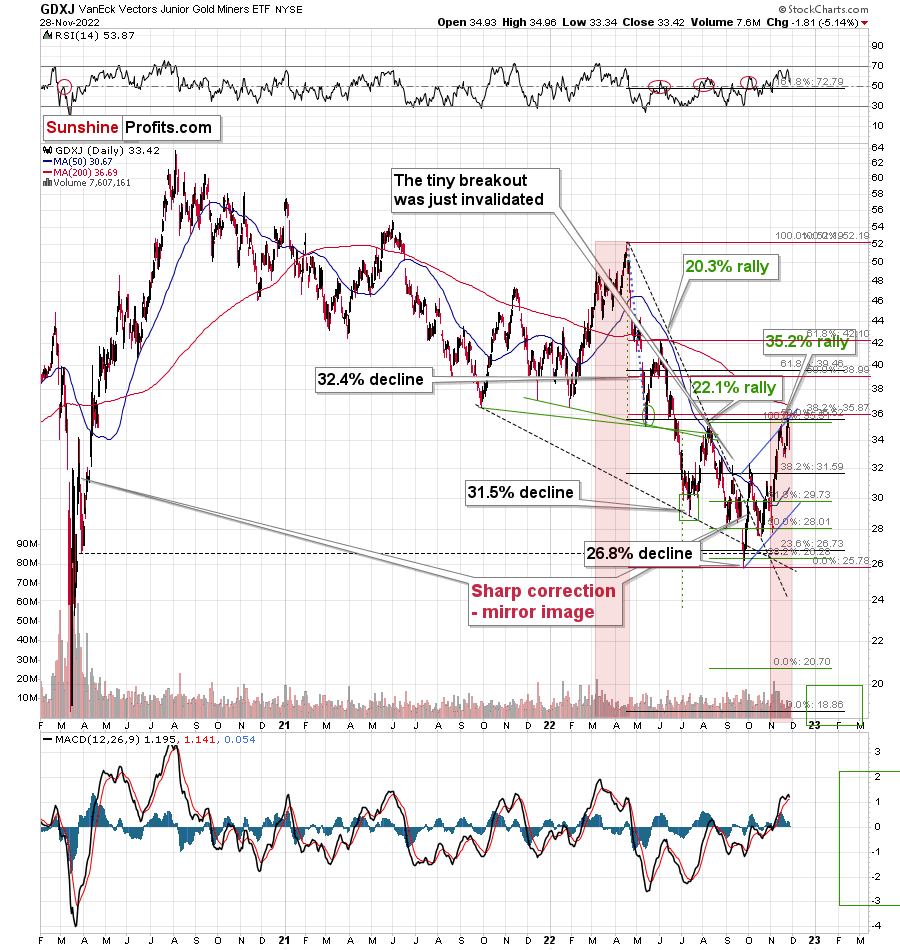

I previously compared the current situation to the one from March and April 2022 in the following way:

The ETF moved higher on Wednesday and then lower on Friday. Most importantly, it moved in near-perfect tune with how it had moved earlier this year – in March and April.

I marked both situations with red rectangles. The initial rally was accompanied by huge volume, which then waned over the following days and weeks. That’s pretty much what we saw in November – and earlier this year.

Moreover, the GDXJ touched its upper border of the flag pattern once again. It also touched the resistance levels provided by the previous highs (moved slightly above them) and the 38.2% Fibonacci retracement level based on the entire 2022 decline.

This means that the top is likely in or at hand.

Juniors just moved back below their previous November high as well as back below their August high. This invalidation – similarly to the invalidation in stocks – suggests that lower values of mining stocks are likely just around the corner.

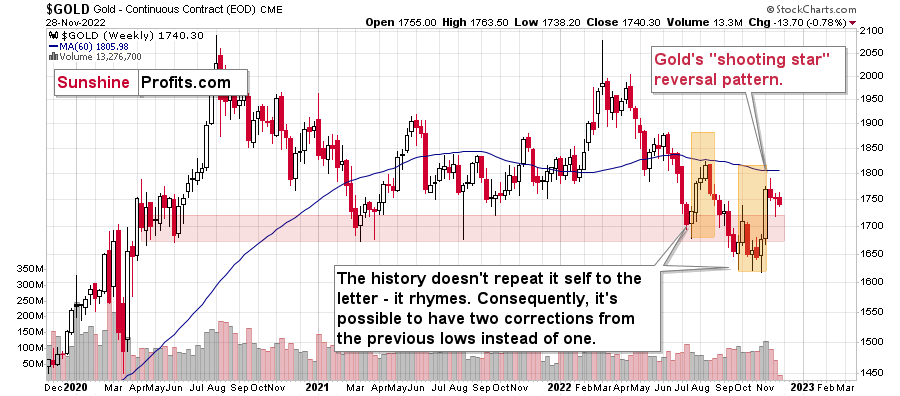

What about gold’s outlook?

Well, gold is behaving just like it was likely to after the powerful weekly reversal that we saw a bit over a week ago.

Last week it reversed to the upside, but the volume on which it did so was weak, so it wasn’t believable.

And indeed, this week gold is moving lower.

What’s next? As stocks are likely about to slide, and so is gold, the prices of mining stocks are likely to tumble – rather sooner than later.

Having said that, let’s take a look at the markets from a more fundamental point of view.

Hawkish Realities

With the S&P 500 suffering on Nov. 28, liquidity-fueled assets have succumbed to traders’ wrath; and with the silver price declining sharply as well, the price action highlights how the crowd is often the most bearish at the bottom and the most bullish at the top. To explain, I wrote on Nov. 15:

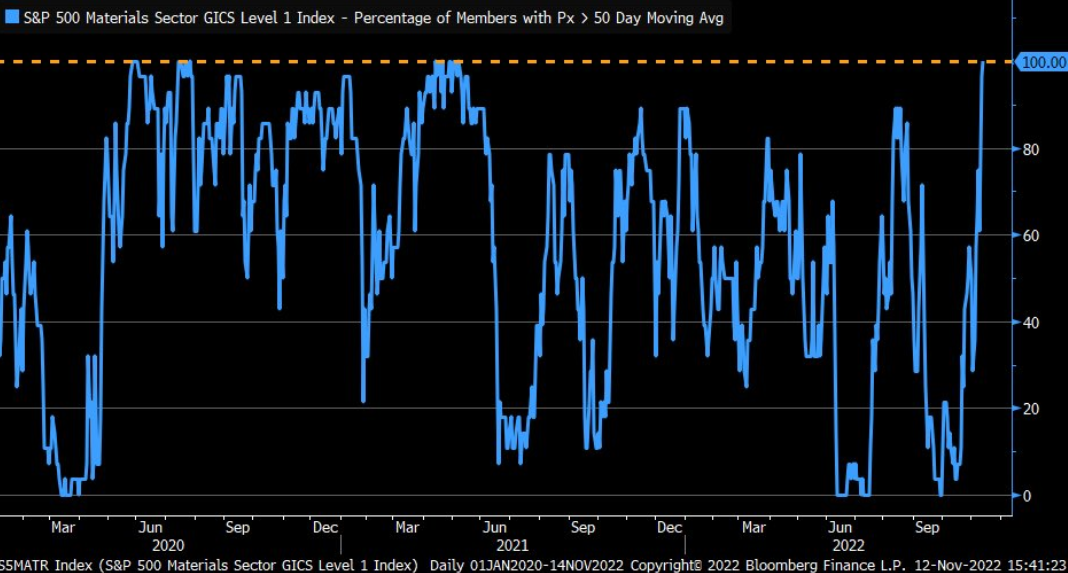

While CNN’s Fear & Greed Index signals greed, though, it’s still below extreme greed, the materials sector is on another level.

Please see below:

To explain, the blue line above tracks the percentage of companies in the materials sector trading above their 50-day moving average. For context, metals and mining make up roughly 14% of the sector. If you analyze the right side of the chart, you can see that the figure stands at 100%, which is a sizable shift from the 0% present in late September.

As a result, the data highlights why we’re likely much closer to the top than the bottom; and notice how abnormally high and low readings are nearly impossible to sustain? This is because periods of too much pessimism and optimism often revert to the average when investors take a thoughtful look at the fundamentals.

Therefore, since the metric can’t go any higher, a material reversal should result in substantial declines for gold, silver and mining stocks over the medium term.

So, while a substantial decline should commence in the months ahead, the fervent flows into the materials sector was a bearish sign that often haunts the momentum investors.

Please see below:

To explain, the candlesticks above track the silver futures price and the vertical gray line represents the price action on Nov. 14. As you can see, silver hit an intraday high on Nov. 15, and the upward momentum has stalled ever since.

Thus, while bearish positioning and short covering helped ignite the recent upswing, the backdrop is now materially different, and the bullish trade has become crowded. Furthermore, if (when) hawkish realities weigh on risk assets, the silver price should be a major casualty.

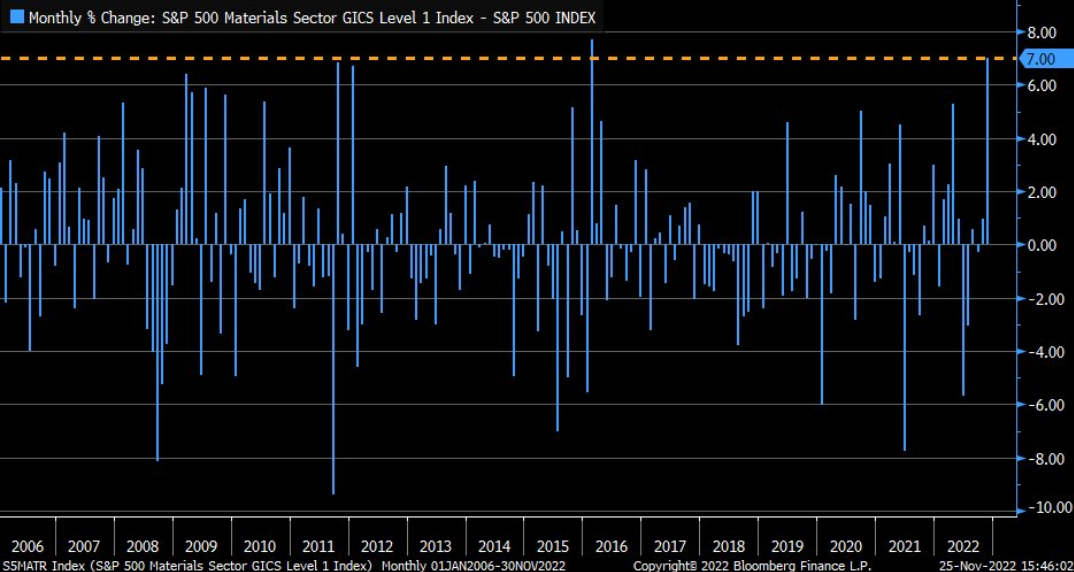

As further evidence, the materials sector's outperformance of the S&P 500 this month is one of the greatest since 2006 (as of Nov. 25).

Please see below:

To explain, the blue bars above track the monthly change in the performance spread between the materials sector and the S&P 500. If you analyze the right side of the chart, you can see that the former has outpaced the latter by 7%.

More importantly, the horizontal yellow line at the top shows how the magnitude of the monthly outperformance is the second-largest since 2006. As such, it’s another example of how investors’ overenthusiasm had them piling into assets like silver even as the fundamentals remained profoundly bearish; and since great dispersions often precede great reversions, the silver price is highly vulnerable to a sharp decline if (when) sentiment shifts.

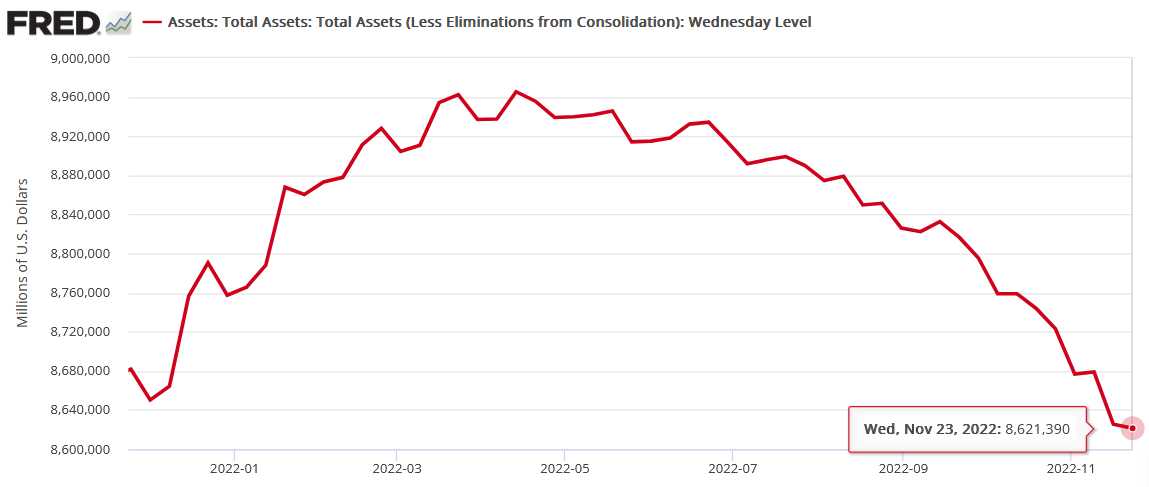

Also, please remember that rate hikes are not the only fundamental problem confronting the silver price. With quantitative tightening (QT) continuing to accelerate, the Fed’s balance sheet hit a new 2022 low on Nov. 23 (updated on Nov. 25). Consequently, while record low real interest rates and unprecedented liquidity helped fuel the silver price in the summer of 2020, the current fundamental environment couldn’t be more different.

Valuation Matters

While the S&P 500 sold off on Nov. 28, the damage is relatively mild when considering the recent rally. However, I’ve noted the importance of real interest rates for many months, and the bearish implications for the S&P 500 and the GDXJ ETF remain the same.

Please see below:

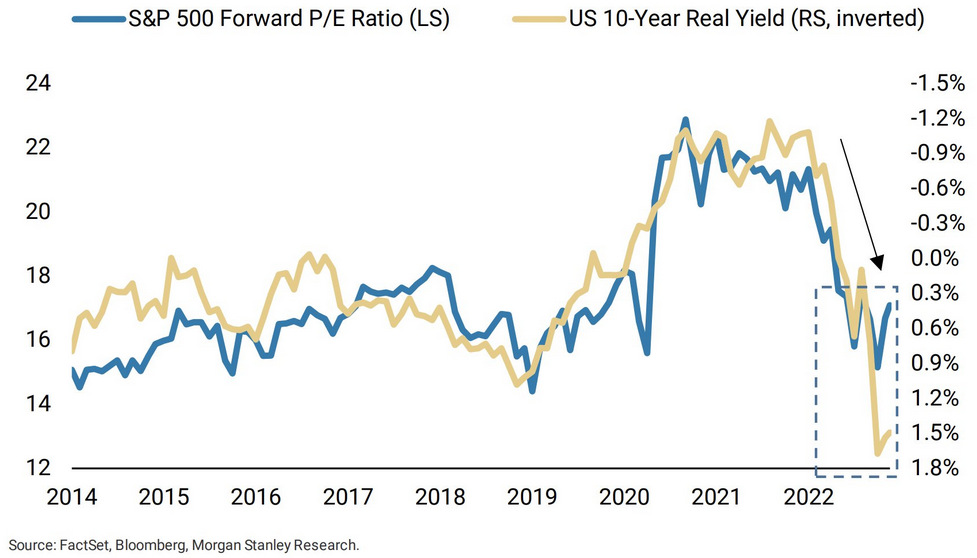

To explain, the blue line above tracks the S&P 500’s forward price-to-earnings (P/E) ratio, while the tan line above tracks the inverted (down means up) U.S. 10-Year real yield. If you analyze the relationship, you can see that a higher U.S. 10-Year real yield often results in a lower S&P 500 forward P/E.

In addition, the gap on the right side of the chart shows that the S&P 500’s forward P/E should be closer to ~13, not ~17; and while seasonality is bullish, the medium-term fundamentals are highly bearish because the U.S. 10-Year real yield has likely not seen its peak. For context, I wrote on Oct. 7:

The U.S. 10-Year real yield often peaks alongside the FFR (or near it). As a result, with the Fed poised to raise the FFR by at least another 1.25% (to reach 4.5%), the U.S. 10-Year real yield should have more room to run, which is bullish for the USD Index.

Please see below:

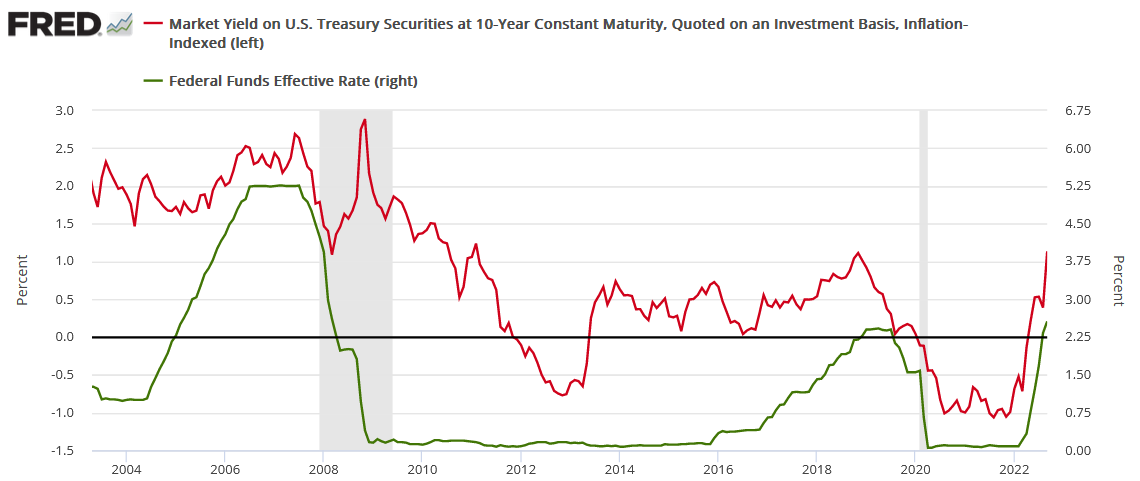

To explain, the red line above tracks the U.S. 10-Year real yield, while the green line above tracks the FFR. As you can see, a higher FFR supports higher real interest rates. Also, when the FFR hit ~4.5% in February 2006, the U.S. 10-Year real yield reached a monthly high of 2.14%, and it occurred with a YoY CPI at roughly half the current rate.

Therefore, while the U.S. 10-Year real yield is still a long way from 2.14%, please remember that the Fed needs higher real interest rates to curb inflation. Consequently, the S&P 500’s already overvalued forward P/E should come under more pressure in the months ahead; and as earnings decelerate due to the Fed’s war on demand, a lower P/E multiple and weaker earnings should make the bulls extremely uncomfortable in 2023.

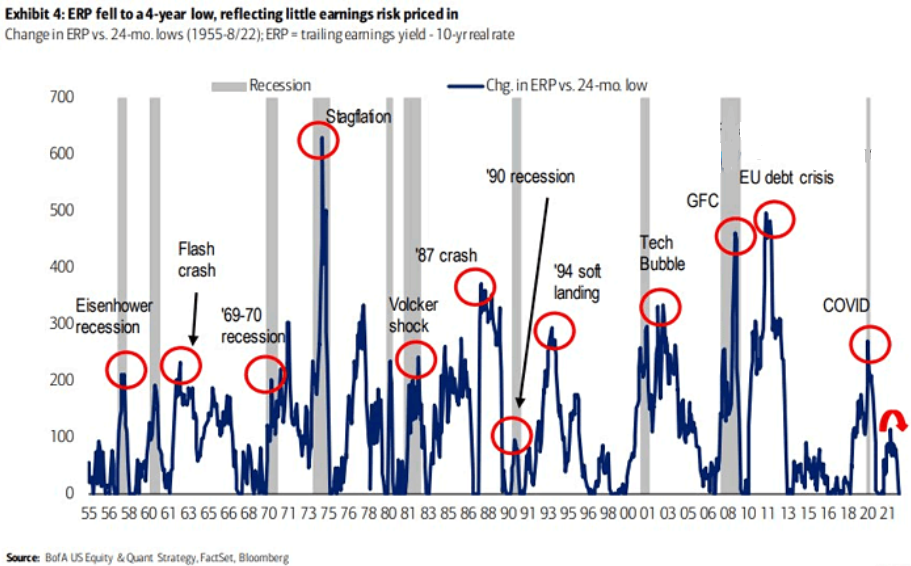

On top of that, the equity risk premium (ERP) is another important metric that highlights investors’ misguided faith in the Fed.

Please see below:

To explain, the blue line above tracks the change in the ERP relative to its 24-month low. If you analyze the annotations, you can see that historical crises often result in sharp spikes in the ERP. However, the low reading on the right side of the chart shows how the ERP is priced like we’re in a bull market with little fundamental risk.

As a result, with a recession poised to commence in 2023, and prior recessions seeing material spikes in the ERP, investors’ sanguine attitudes should vanish as the fundamentals continue to deteriorate.

Finally, while Morgan Stanley sees the S&P 500 ending 2023 at 3,900, Chief U.S. Equity Strategist Mike Wilson expects plenty of volatility before a bottom materializes in Q1 2023.

Please see below:

To explain, Wilson’s base case 3,900 target for the S&P 500 at year-end 2023 assumes a slide to ~3,300 in Q1, as recession fireworks erupt. In the bear case, the low could approach ~3,000, and in the bull case, ~3,500. Thus, while he remains relatively optimistic about the long-term outlook, the S&P 500’s valuation imbalance makes the medium-term outlook much more treacherous.

The Bottom Line

While risk appetite wobbled on Nov. 28, the dip buyers are unlikely to go down without a fight. But, with the medium-term technicals and fundamentals still profoundly bearish, their resolve should wane as reality sets in. Moreover, with the USD Index and the U.S. 10-Year real yield both rising on Nov. 28, their strength supports lower prices for gold, silver and mining stocks; and with tighter financial conditions needed to cool inflation, the USD Index and the U.S. 10-Year real yield should hit new highs in the months ahead.

In conclusion, the PMs declined on Nov. 28, as the pivot narrative continues to unwind. Furthermore, while I warned that the prospect of a dovish 180 was ridiculous, asset prices are still far from reflecting this fundamental reality. Therefore, more downside should confront the PMs before long-term buying opportunities emerge.

Overview of the Upcoming Part of the Decline

- It seems to me that the corrective upswing is over (or about to be over) and that the next big move lower is already underway (or that it’s about to start).

- If we see a situation where miners slide in a meaningful and volatile way while silver doesn’t (it just declines moderately), I plan to – once again – switch from short positions in miners to short positions in silver. At this time, it’s too early to say at what price levels this could take place and if we get this kind of opportunity at all – perhaps with gold prices close to $1,500 - $1,550.

- I plan to switch from the short positions in junior mining stocks or silver (whichever I’ll have at that moment) to long positions in junior mining stocks when gold / mining stocks move to their 2020 lows (approximately). While I’m probably not going to write about it at this stage yet, this is when some investors might consider getting back in with their long-term investing capital (or perhaps 1/3 or 1/2 thereof).

- I plan to return to short positions in junior mining stocks after a rebound – and the rebound could take gold from about $1,450 to about $1,550, and it could take the GDXJ from about $20 to about $24. In other words, I’m currently planning to go long when GDXJ is close to $20 (which might take place when gold is close to $1,450), and I’m planning to exit this long position and re-enter the short position once we see a corrective rally to $24 in the GDXJ (which might take place when gold is close to $1,550).

- I plan to exit all remaining short positions once gold shows substantial strength relative to the USD Index while the latter is still rallying. This may be the case with gold prices close to $1,400 and GDXJ close to $15 . This moment (when gold performs very strongly against the rallying USD and miners are strong relative to gold after its substantial decline) is likely to be the best entry point for long-term investments, in my view. This can also happen with gold close to $1,400, but at the moment it’s too early to say with certainty.

- The above is based on the information available today, and it might change in the following days/weeks.

You will find my general overview of the outlook for gold on the chart below:

Please note that the above timing details are relatively broad and “for general overview only” – so that you know more or less what I think and how volatile I think the moves are likely to be – on an approximate basis. These time targets are not binding nor clear enough for me to think that they should be used for purchasing options, warrants, or similar instruments.

Summary

Summing up, last week’s shooting star reversal candlestick in gold already resulted in lower gold prices, and as Bitcoin forms its short-term bottom, the big decline in the precious metals sector (especially in junior mining stocks) is likely to resume.

I would like to take this opportunity to congratulate you on your patience with this trade (and I’m grateful for your understanding that not every corrective upswing can be “caught” in trading terms). Many investors and traders panic and get out of the market exactly at the wrong time, but your patience and self-discipline mean that you’re poised to make the most of what the market brings us this and next year.

Moving back to the market, it appears to be yet another time when the markets are incorrectly expecting the Fed to make a dovish U-turn, and based on this, the part of the 2008 decline where we saw the biggest corrective upswing materialized.

In my opinion, the current trading position is going to become profitable in the following weeks, and quite possibly in the following days. And while I can’t promise any kind of performance, I fully expect it to become very profitable before it’s over and to prolong our 2022 winning streak.

After the final sell-off (that takes gold to about $1,350-$1,500), I expect the precious metals to rally significantly. The final part of the decline might take as little as 1-5 weeks, so it's important to stay alert to any changes.

To summarize:

Trading capital (supplementary part of the portfolio; our opinion): Full speculative short positions (300% of the full position) in junior mining stocks are justified from the risk to reward point of view with the following binding exit profit-take price levels:

Mining stocks (price levels for the GDXJ ETF): binding profit-take exit price: $20.32; stop-loss: none (the volatility is too big to justify a stop-loss order in case of this particular trade)

Alternatively, if one seeks leverage, we’re providing the binding profit-take levels for the JDST (2x leveraged). The binding profit-take level for the JDST: $27.87; stop-loss for the JDST: none (the volatility is too big to justify a SL order in case of this particular trade).

For-your-information targets (our opinion; we continue to think that mining stocks are the preferred way of taking advantage of the upcoming price move, but if for whatever reason one wants / has to use silver or gold for this trade, we are providing the details anyway.):

Silver futures downside profit-take exit price: $12.32

SLV profit-take exit price: $11.32

ZSL profit-take exit price: $74.87

Gold futures downside profit-take exit price: $1,504

HGD.TO – alternative (Canadian) 2x inverse leveraged gold stocks ETF – the upside profit-take exit price: $18.47

HZD.TO – alternative (Canadian) 2x inverse leveraged silver ETF – the upside profit-take exit price: $46.87

Long-term capital (core part of the portfolio; our opinion): No positions (in other words: cash)

Insurance capital (core part of the portfolio; our opinion): Full position

Whether you’ve already subscribed or not, we encourage you to find out how to make the most of our alerts and read our replies to the most common alert-and-gold-trading-related-questions.

Please note that we describe the situation for the day that the alert is posted in the trading section. In other words, if we are writing about a speculative position, it means that it is up-to-date on the day it was posted. We are also featuring the initial target prices to decide whether keeping a position on a given day is in tune with your approach (some moves are too small for medium-term traders, and some might appear too big for day-traders).

Additionally, you might want to read why our stop-loss orders are usually relatively far from the current price.

Please note that a full position doesn't mean using all of the capital for a given trade. You will find details on our thoughts on gold portfolio structuring in the Key Insights section on our website.

As a reminder - "initial target price" means exactly that - an "initial" one. It's not a price level at which we suggest closing positions. If this becomes the case (as it did in the previous trade), we will refer to these levels as levels of exit orders (exactly as we've done previously). Stop-loss levels, however, are naturally not "initial", but something that, in our opinion, might be entered as an order.

Since it is impossible to synchronize target prices and stop-loss levels for all the ETFs and ETNs with the main markets that we provide these levels for (gold, silver and mining stocks - the GDX ETF), the stop-loss levels and target prices for other ETNs and ETF (among other: UGL, GLL, AGQ, ZSL, NUGT, DUST, JNUG, JDST) are provided as supplementary, and not as "final". This means that if a stop-loss or a target level is reached for any of the "additional instruments" (GLL for instance), but not for the "main instrument" (gold in this case), we will view positions in both gold and GLL as still open and the stop-loss for GLL would have to be moved lower. On the other hand, if gold moves to a stop-loss level but GLL doesn't, then we will view both positions (in gold and GLL) as closed. In other words, since it's not possible to be 100% certain that each related instrument moves to a given level when the underlying instrument does, we can't provide levels that would be binding. The levels that we do provide are our best estimate of the levels that will correspond to the levels in the underlying assets, but it will be the underlying assets that one will need to focus on regarding the signs pointing to closing a given position or keeping it open. We might adjust the levels in the "additional instruments" without adjusting the levels in the "main instruments", which will simply mean that we have improved our estimation of these levels, not that we changed our outlook on the markets. We are already working on a tool that would update these levels daily for the most popular ETFs, ETNs and individual mining stocks.

Our preferred ways to invest in and to trade gold along with the reasoning can be found in the how to buy gold section. Furthermore, our preferred ETFs and ETNs can be found in our Gold & Silver ETF Ranking.

As a reminder, Gold & Silver Trading Alerts are posted before or on each trading day (we usually post them before the opening bell, but we don't promise doing that each day). If there's anything urgent, we will send you an additional small alert before posting the main one.

Thank you.

Przemyslaw K. Radomski, CFA

Founder, Editor-in-chief