A lot has been going on in Europe in the first two months of 2015. The Swiss National Bank removed the peg of 1.20 francs per euro and the European Central Bank announced the QE program. Then radical left-wing Syriza won the elections in Greece and announced that it wants to renegotiate the bailout plan with the hated troika. Soon after Sweden joined a growing group of countries to cut its key interest rate to negative. While the Russian economic crisis aggravated as S&P downgraded (as well as Moody’s a bit later) its credit rating to junk status, the conflict in Ukraine continued, although the ceasefire was eventually agreed upon.

All of these events were covered in Gold News Monitors, and in the March edition of Market Overview we cover all of them, however in this article we will focus on one of them in greater detail – the situation in Greece.

A few days after launching the European QE, investors’ attention moved from Frankfurt to Athens, where Syriza triumphed in general elections. The new government opposed an extension of the bailout program that ended February 28 under the bailout terms being in force at that time. Instead, Prime Minister Alexis Tsipras and his finance minister Yanis Varoufakis, called for a bridge loan to give Greece more time to renegotiate a deal. Not surprisingly, the troika of lenders (the IMF, the ECB and the EU), which owes 76 percent of a €323 billion-worth Greek debt, did not understand Greece’s anti-austerity stance.

Why? Greece has already received two large bailouts, which actually enabled it to buy some time, delay austerity and continue policy of deficits. The truth is that the “austerity” in Hellas is a myth. Even though the government cut its spending (however, in relation to GDP it is even higher than before the Eurozone crisis), it did not conduct structural reforms or adjust its economy, as other peripheral countries partially did. The debt burden is also not so high, in the 2014 interest spending amounted to 2.6 percent of GDP (in 2015 it is estimated at 1.5 percent), much lower than several less indebted European countries pay, actually.

However, the Greece tough course was quite understandable (abstracting from the Syriza’s promises to voters and the strategic position of the country in NATO), because the country ran a primary surplus (so, without the interest payments component, it had a positive budget balance). It means that the government was able to finance its expenditures only through taxes (and something was even left over and could be used to pay interest), which naturally strengthened the temptation to default.

Finally, the Greek government has eventually reached an agreement with its creditors, as we had believed. The bailout program for Greece was extended by four months in return for a commitment to honor its debt obligations and conduct structural reforms, which Greece and creditors will agree to by the end of April (the list of reforms proposed by the Greek government was initially backed by the European Commission). Although Greece could prepare its own list of reforms and negotiated a smaller primary surplus, the agreement signed just a few days before the Greek banks would have been broke, reveals that Greek deposit flight is on a trigger-sensitive path at any moment.

Indeed, this was a strong argument for reaching an agreement. The banks’ condition was significantly deteriorating, as depositors were withdrawing their capital from the domestic banks and shifting it abroad. Greeks feared an exit from the Eurozone, which could entail their savings to be converted to devaluated drachma. Consequently, the Greek banks lost over €20 billion in just the first two months of 2015, which meant that the country’s financial system would be broke without reaching an agreement and ECB extending support. This is why we believed that both sides would finally reach a deal – otherwise Greece would simply run of money and its banking system would be demolished.

The fiscal situation has also significantly deteriorated since the end of 2014. In January the tax revenues fell by 16 percent compared to year earlier, a loss of €775 millions in just one month. The decrease in tax receipts was caused by the drop in consumption, big hikes in taxes last year and an increase in tax evasion (partially due to hikes and partially due to expectations of tax cuts promised by the Syriza).

The deal between Greece and its creditors eases tensions and the risk of Grexit, and decreasing tensions which would be negative for the gold market in the short run. However it is only a pause in a drama, because between Greece has to repay €11 billion in the coming months(as some of its debt matures), €6.7billion from that sum after April (in July and August), which would be a rather impossible task without a fresh bailout program.

It means that the February agreement was only a means of buying time. Greece’s problems were not solved, but only postponed for four months. If the bailout program is not extended in April, the Greek government will have to default on its debt. According to the Greek government itself, it can pay the bills until June when the bonds held by the ECB worth €3.5bn mature. Although the sole default on the state obligations does not automatically entail leaving the Eurozone, the problem is that Greek banks depend on help from the ECB. (This is why we do not consider potential help from Russia or China as possible. Abstracting from their own financial problems and rather not their area of influence, the sum needed by the Greek banks is too big, which means that the ECB is the only possible backstop for Greek banks). Therefore, if the banks were cut off by the ECB, the government would be forced to return to the drachma in order to fund the local banks. And if the bank runs and capital outflows repeat in a similar scale, Hellas may also introduce capital controls.

What are the possible consequences of the Grexit for the global economy and gold market? Such worst-case scenarios would result in the increase of market uncertainty about the contagion effects and the future of the Eurozone. The opinions on the possible impact of Grexit on markets are very mixed. For example, the German government believes (however, it could be a bluff) that the Eurozone is now in much better shape than in 2012 and would be able to cope with Grexit with limited contagion.

The consequences are very difficult to predict, but it is worth pointing that the very construction of the Eurozone (one central bank and several independent governments) is inherently flawed and unstable. The Grexit will deepen the Eurozone debt problem, which was never solved, for sure. It would be a precedent that could encourage other members to leave. There is also a risk of a repetition of the contagion of 2011 and 2012, when a few other peripheral countries got bailouts. This is what many investors were afraid of in February, which induced them to accept even negative interest rates in betting against the euro or the breakdown of the Eurozone.

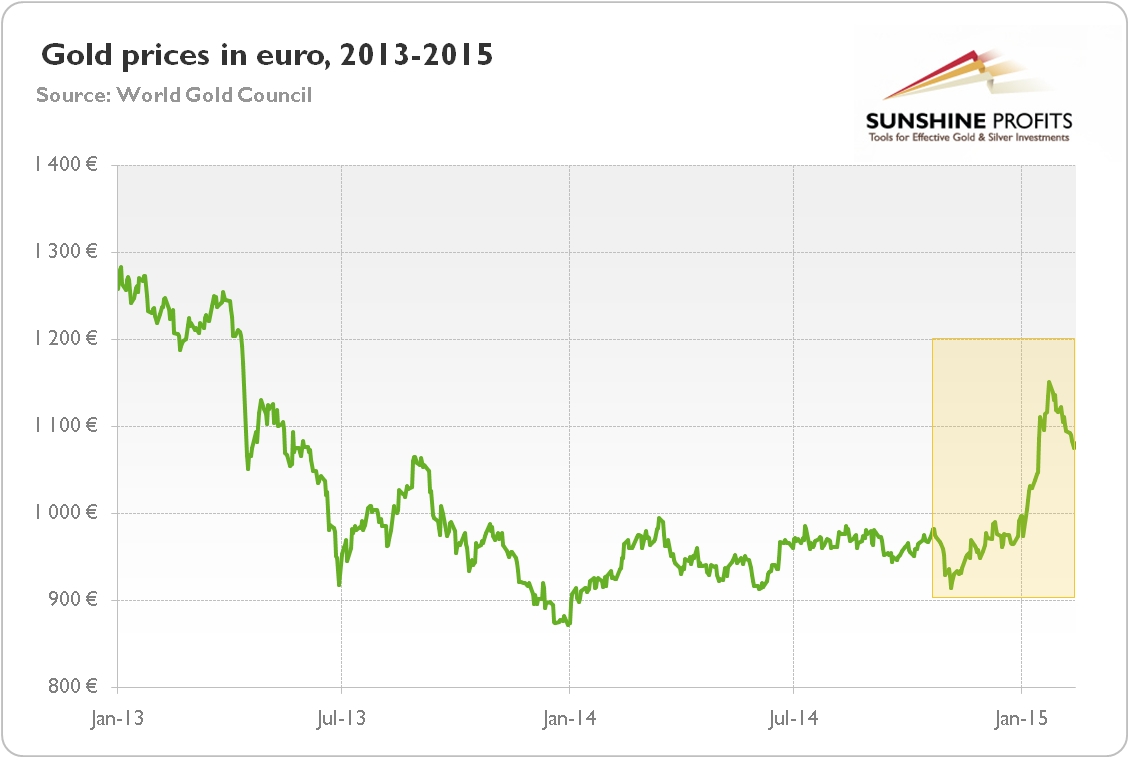

Graph 1: Gold prices in euro from January 2013 to February 13, 2015

The demand for gold as a safe-haven (especially of Greeks faced with devaluation) should significantly rise then. Indeed, there has been a noticeable increase in demand for gold coins in Greece in the last quarter of 2014 and at the beginning of 2015. And the gold prices in terms of the euro have gone parabolic in the last few months (Figure 4), however the rise in gold prices in terms of the U.S. dollar may be hampered a bit due to possible parallel strengthening of the greenback.

We focus on the global economy and fundamental side in our monthly Market Overview reports; however we provide also Gold & Silver Trading Alerts for traders interested more in the short-term prospects. Sign up for our mailing list and stay up-to-date. It's free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview