Last week, we covered three important reports about the gold market. Today, we would like to discuss yet another publication. On March 31, the World Gold Council (WGC) released a market update entitled “Gold in a world of negative interest rates”. What are the main conclusions of the report?

NIRP Will Structurally Increase Demand for Gold

The price of gold rose 16.7 percent in U.S. dollars in Q1 2016, partially due to NIRP, according to the WGC. The report mentions four reasons why the negative interest rates will structurally increase the demand for gold. First, NIRP reduces the opportunity cost of holding gold. Second, it limits the pool of assets some investors would invest in. Third, NIRP erodes confidence in fiat currencies due to the threat of currency wars and monetary interventions. Fourth, negative interest rates increase uncertainty and market volatility as central banks run out of effective policy options to combat inflation/deflation and/or spur growth.

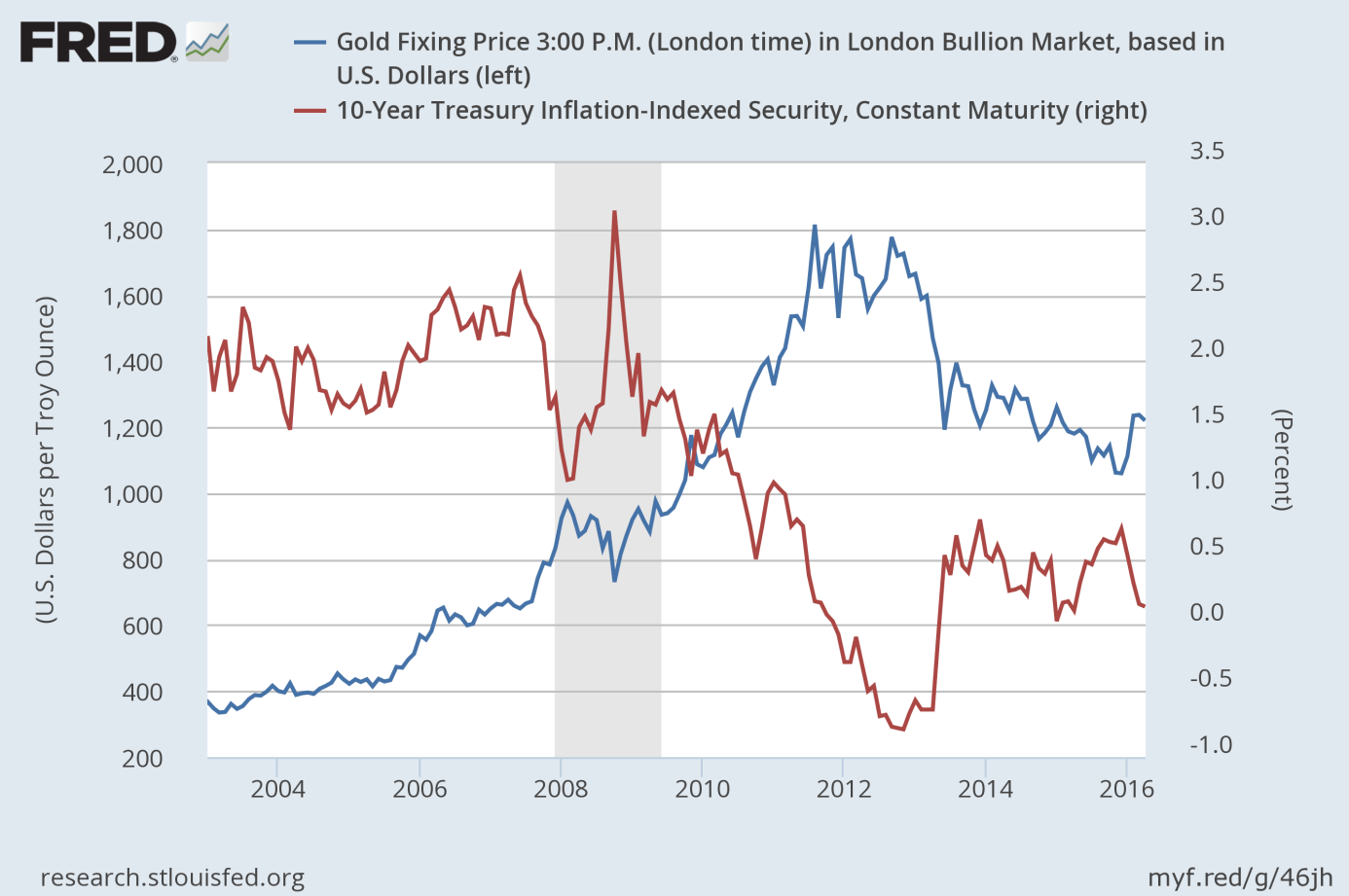

We agree with the WGC. We wrote repeatedly that real interest rates are a significant driver of gold prices. Actually, as one can see in the chart below, the movements in the gold prices mirror changes in real interest rates.

Chart 1: The price of gold (blue line, left axis, London P.M. fix) and real interest rates (red line, right axis, 10-year inflation-indexed Treasuries) from 2003 to April 7, 2016.

The yellow metal usually shines when real interest rates are low and tends to appreciate significantly during periods of negative real interest rates (the WGC estimates that “when real rates are negative, gold returns tend to be twice as high as the long term average”). This is because when real interest rates are negative, creditors are losing money, therefore they are more prone to buy gold, even it does not bear interest or dividends. The example which confirms the adverse relationship between real interest rates and gold prices may be the period after the recent global financial crisis. Real interest rates started falling in late 2008, while gold rallied. Real interest rates dived below zero in late 2011, when gold was at its heights. On the contrary, real interest rates started increasing in late 2012, so the price of gold entered a bear market soon. Therefore, the negative interest rates policy, if it translates into negative market rates, might be fundamentally bullish for gold prices.

NIRP Reduces Investable Pool of Assets

The WGC reports that in the current negative nominal interest-rate environment, about 30 percent of high quality sovereign debt (more than US$8 trillion) is trading with negative yields. According to the WGC, in such a setting some investors, especially pension funds, are likely to increase their holdings in gold. It makes sense, since holding bonds with negative nominal interest rates is a loss-making strategy, unless the interest rates will continue to fall. In other words, buying negative yielding bonds implies a guaranteed loss if they are held to maturity. Investors can make a profit as long as they are able to find a ‘greater fool’ who will buy the securities at a higher price (and lower yield) in hope that the central banks will keep pushing rates further below zero. Although Einstein once said that human stupidity is infinite, the practice shows that the ‘greater fool’ strategy is unstable in the long-term.

Conclusions

The key takeaway is that the NIRP is fundamentally bullish for the price of gold, as it may structurally increase the demand for the shiny metal. NIRP reduces the opportunity cost of holding gold and the pool of assets some investors would be willing to hold, and erodes confidence in central banks and fiat currencies. In consequence, the portfolio analysis conducted by the WGC suggests that gold allocations in a low rate environment should be more than twice their long term average. We agree that under NIRP bonds may not be so effective in balancing equity risk as in normal times, and some investors may need to rebalance their portfolios by increasing gold holdings, however, the optimal allocation to gold depends on the exact investment objectives and composition of individual portfolios.

Disclaimer: Please note that the aim of the above analysis is to discuss the likely long-term impact of the featured phenomenon on the price of gold and this analysis does not indicate (nor does it aim to do so) whether gold is likely to move higher or lower in the short- or medium term. In order to determine the latter, many additional factors need to be considered (i.e. sentiment, chart patterns, cycles, indicators, ratios, self-similar patterns and more) and we are taking them into account (and discussing the short- and medium-term outlook) in our trading alerts.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview