Based on the July gold Market Overview report.

Believe it or not, we are finally witnessing a true monetary revolution. Unfortunately it is not the one that gold bugs have long waited for. Quite the opposite. We have the so called “monetary cranks” governing one of the most important central banks in the world. People who set the interest rates not at very low, not even at zero, not even at negative real interest rates, but at negative nominal interest rates. Hold your horses and constrain your joy – this does not concern the interest rate on your loan. It is the interest rate for the deposit facility at the central bank.

Of course it is not something that hasn’t happened previously, or something completely unexpected. Europeans apparently got tired of Americans always leading the way and having the final revolutionary word. Hence the Europeans went forth with a further step and introduced a NIRP policy – negative interest rate policy. Commercial banks, which are supplying the money to the deposit facility, take out less money than they put in. The interest rate is currently at minus 0,1%.

Why do we refer to the so called “monetary cranks” group? Hard money theorists, believers in commodity money (often gold), coined the term “monetary crank”. The epithet was addressed at those monetary theorists who neglected basic functions of money and the interest rate market. They hated gold for various reasons, but the most important one was that it cannot be increased at will, and as a consequence a positive real interest rate is possible. Cranks proposed to destroy this system by the introduction of purely fictitious money which can be increased at will in favor of particular interest groups.

Let us read the official ECB statement:

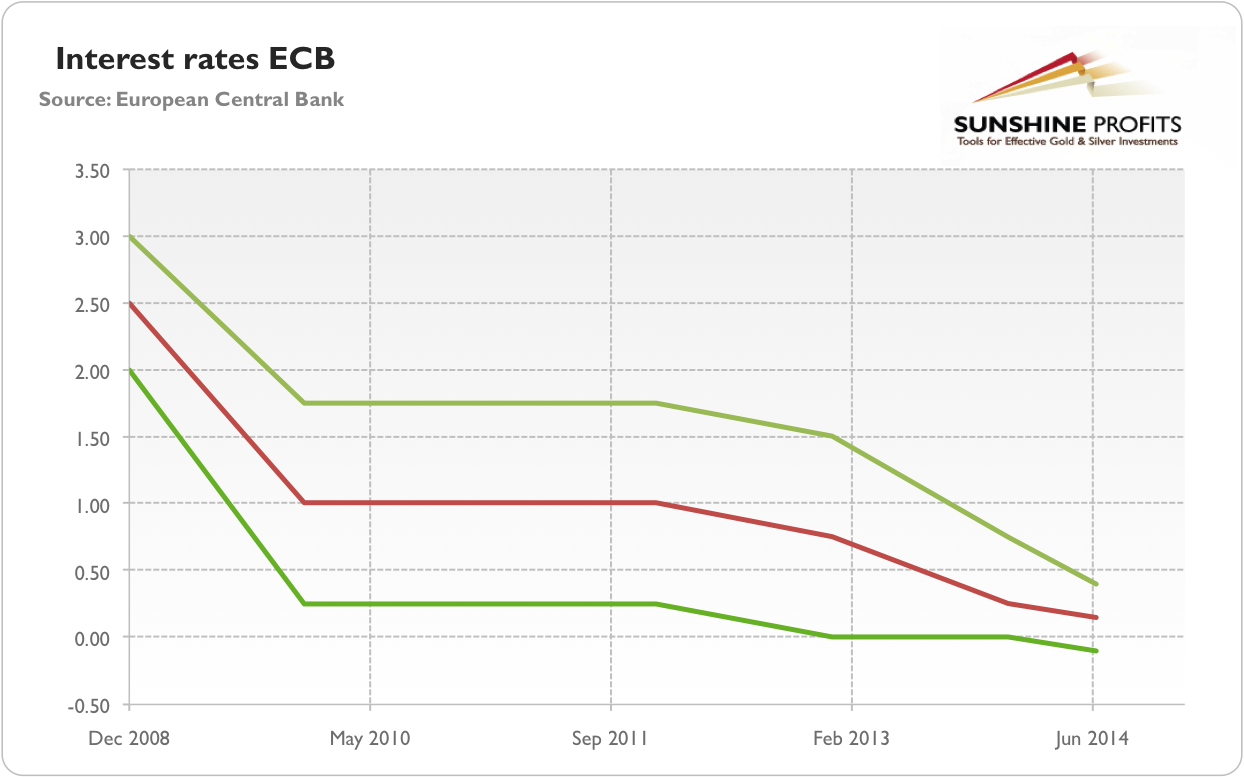

Since euro area inflation is expected to remain considerably below 2% for a prolonged period, the ECB's Governing Council has judged that it needs to lower interest rates. The ECB has three main interest rates on which it can act: the marginal lending facility for overnight lending to banks, the main refinancing operations and the deposit facility. The main refinancing rate is the rate at which banks can regularly borrow from the ECB while the deposit rate is the rate banks receive for funds parked at the central bank. All three rates have been lowered.

To maintain a functioning money market in which commercial banks lend to each other, these rates cannot be too close to each other. Since the deposit rate was already at 0% and the refinancing rate at 0.25%, a cut in the refinancing rate to 0.15 % meant the deposit rate was lowered to − 0.10 % to maintain this corridor.

It was the main feature during sovereign debt crises that banks diverted from the government debts and decided to keep their funds away from them (the threatened ones). Record sums of euros were put into overnight accounts. ECB wants to avoid that and punish (nominally) those banks which are getting to be interested in this option. Moreover since the main refinancing facility has decreased very close to zero, the Bank is eager to move a bit to a lower rate keeping away from it.

In reality the move appears to be as much desperate as ineffective. Almost like a decision to highly tax strawberries with high hopes to stimulate the market for bananas. Banks’ decisions not to be engaged and launch into new monetary expansion is not something irrational. It is a well thought decision to be cautious and it is partially imputed from the behavior of market participants, who currently treat many assets as untrustworthy.

How does this all relate to the gold market? As you already know at Market Overview we firmly believe in the contrarian investment hypothesis for gold. The price of gold is not something strictly related to absolute debt levels, inflation levels, GDP levels, and so forth. Today it is mainly an investment vehicle alternative to the current fiat system with boosted paper assets. As long as the current system suffers deeply from its internal flaws and contradictions, gold shall be a shiny alternative opportunity to invest the money. Henceforth we can answer the question about the importance of negative interest and the price of gold. No doubt changes by the ECB are not a signal that things are going well; the crisis has not been resolved yet. Negative interest for deposit facility indicates that there is still a lot of garbage in the financial market and there are much reduced investment opportunities than were available in the past. Therefore alternative proposals to secure the capital, including gold, look very attractive indeed. ECB just gave us a signal that it is still the case.

The above is a small excerpt from our latest Market Overview report. The full version includes much more in-depth analysis of this and other fundamental factors that are likely to affect the gold market in the future. You can sign up for these reports here.

Thank you.

Matt Machaj, PhD

Sunshine Profits‘ Market Overview Editor