In the last Market Overview we wrote about falling commodity prices and problems of emerging markets resulting from the strong U.S. dollar. In this edition we would like to focus on the Russian economy, which suffers from both problems. Declines in oil prices erase a great deal of government revenue, while at the same time the rise in the U.S. dollar to ruble exchange rate threatens the solvency of indebted banks and companies. Because Russia’s financial instability can affect other markets that lend money to Russian companies, we have to analyze what the wounded eastern bear could really mean to the global economy and gold market.

Economists like to compare the current situation to other problems Russia experienced in the past: the 1998 crisis, the collapse of the Soviet Union or the Great Recession in 2008-2009. In both the past and now the Russian economy has been heavily dependent on oil and gas (the fuel and energy sectors provide a quarter of GDP, and half of government revenue comes from oil and gas exports). The 1970s were a time of rising oil prices (from 1972 and 1981 they almost quintupled) and Soviet expansionism, while the collapse of a communist empire may be traced to the fall in oil prices by around two thirds in 1985 (according to the Yegor Gaidar). That drop in oil prices resulted from the strong dollar policy of Reagan and Volcker and from Saudi Arabia’s cessation of supporting oil prices. In consequence, the Soviet Union was desperately low on hard currencies and in fact collapsed a few years later.

The transition into a market economy was not simple and the process of privatization was deeply corrupted (infamous loans-for-share scheme). Because of tax evasion, large subsidies for the manufacturing firms, a costly war in Chechnya (now we have Crimea and Ukraine) and unsustainable social spending, through 1996-97 the government run budget deficits that amounted to 7-8 percent of GDP. The stabilization of inflation (its rate fell from 131 percent to 11 percent in 1997) fuelled a wave of optimism, leading to an inflow of foreign investment. Capital controls were removed and Russian banks increased their foreign liabilities from 7 percent of their assets in 1994 to 17 percent in 1997, which laid the foundation for the crisis.

The Russian economy suffered from many systemic weaknesses, most notably its unsustainable debt accumulation (interest payments on the debt reached a high of 43 percent of total government revenues in 1998). However the direct triggers of the 1998 crisis were external. In November 1997, after the onset of the Asian crisis, the ruble came under speculative attack and the Central Bank of Russia lost nearly 6 billion U.S. dollars of reserves defending the currency.

Next month the prices of oil and non-ferrous metals, responsible for up to two thirds of hard currency earnings, began to drop. After the Asian crisis investors were risk-averse and feared that the Russian government would devalue the ruble (which had been pegged to the U.S. dollar since 1995 as a tool to fight inflation) or default on debts. Investors soon started withdrawing their capital from Russia. In May, 1998 oil prices dropped to $11 per barrel, less than half their level one year earlier. Government bond yields increased to 47 percent, while CBR hiked the lending rate from 30 to 50 and later to 150 percent to defend the ruble (compare to the hike from December 15, 2014). However, all the steps taken by the government and central bank appeared to be insufficient. August 13, 1998, the Russian security and currency markets collapsed. Four days later, August 17, the government, depleted of foreign reserves, defaulted on its domestic debt and floated the ruble, which fell by 27 percent.

Another currency crisis in Russia occurred from 2008 to 2009. The ruble weakened 35% against the greenback from the onset of the crisis in August 2008 to January 2009. Not surprisingly, it was also a period of a strong U.S. dollar (due to investors’ flight to U.S. Treasuries as a safe haven) and rapid decline (around 70%) in oil prices. That currency crisis passed in February 2009. Most economists indicate that the reverse in U.S. dollar index and oil prices is the reason for the ruble’s strengthening. Another important factor – especially in the context of current events – could be the decline of the monetary base by 22 percent. The fewer rubles in circulation, the more valuable they are.

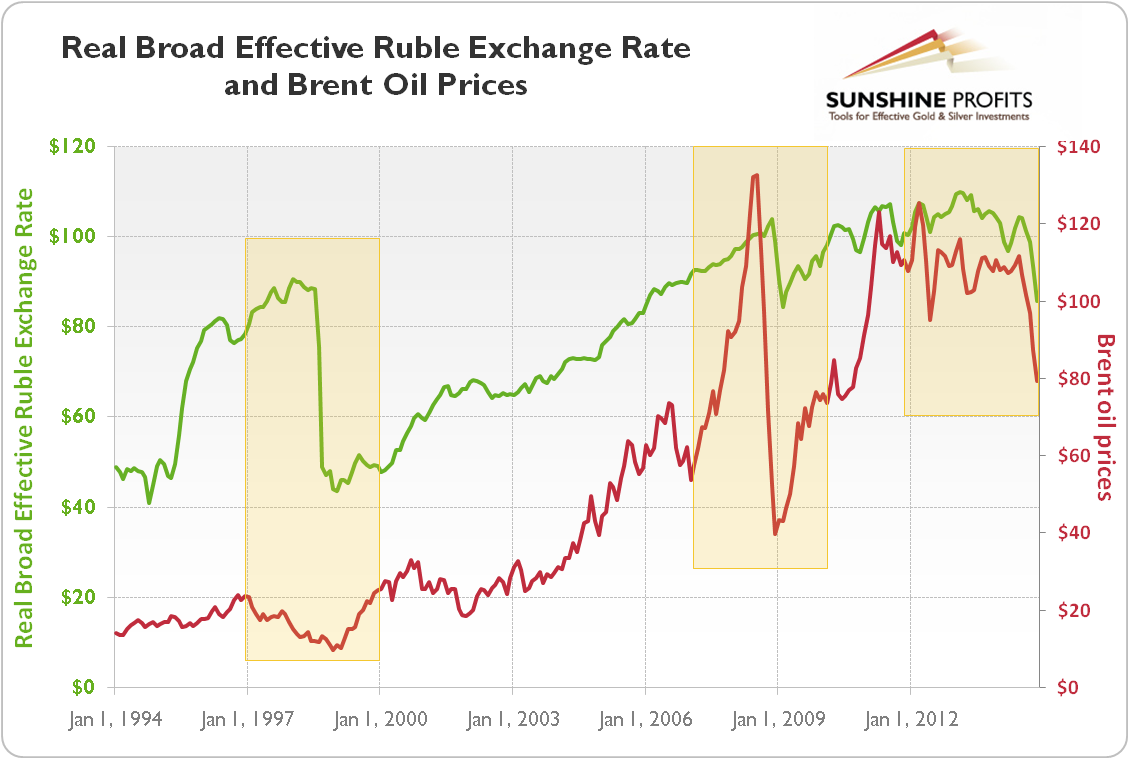

This short history of Russian financial crises proves three things. First, there is a significant positive correlation between ruble and oil prices (which are affected to a large extent by a strong U.S. dollar), as can be seen in Graph 1. Besides the many differences between 1998 and the current situation, the Russian economy is still not developed and suffers from “Dutch disease”. Consequently if oil prices fall, Russian companies don't have as many petrodollars to turn into rubles. There's less demand for rubles overall, so its exchange rate falls.

Graph1: Real broad effective ruble exchange rate (green line) and Brent crude oil prices from 1994 to 2014

Second, the crisis can be solved, but it requires the determined actions of the Central Bank of Russia. Unfortunately, after the infamous Rosneft’s case, its credibility has been called into question, as investors fear that it will be printing more money to help oligarchs’ banks and businesses. Without a credible monetary policy and structural reforms, the Russian economy is going to slump into recession, which will last as long as oil prices do not rise again.

Third, gold prices (in U.S. dollars) did not rise after either the collapse of the Soviet Union, or after the 1998 or 2008-2009 crises, because of an already strong U.S. dollar. Therefore, investors should not expect that the current Russian troubles, no matter how they end, will positively affect the gold prices.

If you’re interested in reading our thoughts on other gold-related topics, we invite you to our website. We focus on the global macroeconomics and fundamental side in our monthly gold Market Overview reports and we provide also Gold Trading Alerts for traders interested more in the short-term prospects. Sign up for our gold newsletter and stay up-to-date. It's free and you can unsubscribe anytime.

Arkadiusz Sieron

Sunshine Profits‘ Market Overview Editor

Gold Trading Alerts

Gold Market Overview