The full version of our analysis (with comments particularly valuable for Precious Metals Traders) is available to our Subscribers. Visit our archives for more gold articles.

As the US industrial output shrank last month for the first time in over a year, it appears certain that the Federal Reserve will decide to release more monetary stimulus on its next policy meeting on November 2-3. A report on Monday revealed that home-builder confidence might have risen this month but it remains worryingly low. According to Paul Ashworth of Capital Economics based in Toronto, "The industrial production report illustrates, if anything, economic growth is still slowing rather than beginning to pick up again, which is yet another reason for the Fed to unleash QE2 (second quantitative easing)".

Industrial output fell by 0.2% in September. Economists have expected to it rise by 0.2%, the same level as August. Overall, it is clear that recovery has slowed dramatically, leaving inflation too low and the unemployment rate too high. Frustration among the unemployed can deal a blow to the Democratic Party in the congressional elections. Most expect the Republicans to gain control over the US House of Representatives as well as win some seats in the Senate.

Questions about the Stimulus Size

While more monetary policy easing is expected, Fed Chairman Ben Bernanke offered little clue as to the size of the asset purchase program. The US stocks ended higher because of better-than-expected performance from Citigroup. In addition, bargain hunters also helped lift the price of government debt. Overall though, financial markets were hardly moved by the recent economic data.

Production at the country's refineries, factories, and mines increased at an annual rate of 4.8& for the third quarter. This is down from 7% in the second quarter. Consumer goods manufacturing declined for the second straight month. Aaron Smith of Moody's Economy.com in Pennsylvania said that, "It reinforces our belief that inventory accumulation has god a little bit ahead of itself and most likely will have to come down and this is going to weigh on output over several months". Meanwhile, utilities output dropped by 1.9% while mining output rose by 0.7% last month.

Gold Forecast

Citing expectations of quantitative easing, Goldman Sachs raised its 12-month forecast for gold to $1,650 an ounce. It also expects long-term interest rates to continue its downward movement. The Goldman Report, authored by Damien Courvalin and David Greely said that, "With the US real interest rates pushing lower off the slowdown in the pace of the US economic recovery and the growing prospect of another round of quantitative easing, we expect gold prices to continue to climb."

The report added that, "Despite the rebound in net speculative length, it remains well below levels consistent with the current low US real interest rate environment." The decline is bound to persist with rates even going lower over the near-term once the Fed undertakes QE measures. As a result, Goldman raised its gold price forecast to $1,400 in three months, $1,525 in six months, and $1,650 in 12 months.

Goldman reports, "The return to quantitative easing will likely be a strong catalyst to drive gold prices higher, and we expect the gold price rally to continue until US monetary policy begins to tighten." This rally, which began in August, was significantly driven by the plummeting yields of 10-year US Treasury Inflation-Protected Securities.

The yield is closer to 0.50% rather than the 1.0% in previous forecasts. Other factors that played a role in gold's continual rise include the demand from central banks and gold exchange-traded funds. However, the bank also added that there is a considerable downside risks associated with gold over the long term, especially once the Fed tightens monetary policy earlier than projected (which we doubt, as at this point "inflating the problems away" appears to be the only viable solution to the economic problems).

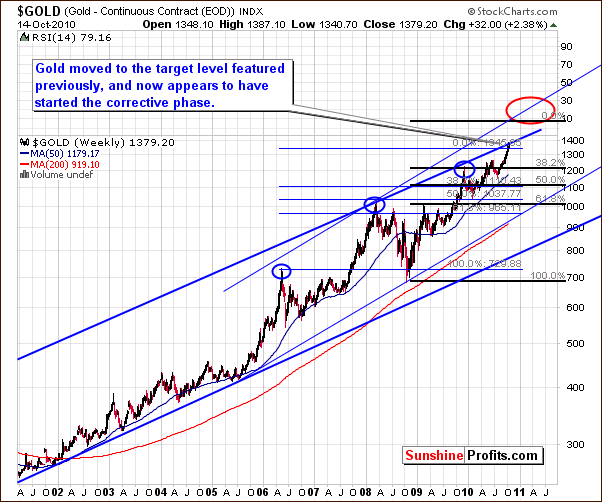

Now, let's take a look at the long-term chart (courtesy of http://stockcharts.com) above. The gold has moved up to the upper borders of the long-term trading channel. However, it looks set for a correction soon. Gold appears incapable of breaking above the resistance line at this point and the rally this week doesn't look like it can delay the correction much longer. Still, once things will have all settled down, another powerful rally is likely to being - perhaps taking gold to $1,500.

Gold vs. Treasuries

Market indications these days are difficult to comprehend. In school, economists were taught that falling 10-year Treasury yield is an indication that the economy can expect a strong currency and low inflation. But right now, the dollar has already fallen 12% since June while the price of gold continues to breach all-time highs. The increasing price of the precious metal is indicating hyperinflation even as bonds are showing warning signs of deflation.

The last time the US experienced severe economic problem was in the late ‘70s and early ‘80s. At the time, the Treasury and the gold market showed better "coordination". Thirty years ago, the Fed's depression of the interest rates led to sharp inflation, a weak dollar, and significant increase in the price of gold. More importantly, Treasury yields skyrocketed as investors demanded better rates for the risks they're taking. Basically, everything made sense.

The environment today is almost the same to the occurrence 30 years ago, except that the 10-year notes plummeted to 2.4% today from 6.6% back in 2000. But other components are the same. For example, the monetary base surged both then and now - this time, instead of doubling over an eight year period, it has tripled in 12 years (from $621 billion in 2000 to $2 trillion today). The dollar price of the yellow metal has quadrupled even as the US dollar dropped 35% of its value.

It is only possible to take advantage of low-interest rates if a country has low inflation, stable monetary policy, high savings rate, and low debt levels. US consumers currently have very low savings rate at 5.8%. Personal savings rate of American consumers have bordered on negligible, sometimes even negative, from 1998 to 2008. With the national debt at 93% and annual deficit at 9% of gross domestic product (GDP), low interest rates may exist over a long timeframe.

For some analyst, it appears that the Federal Reserve wants Americans to anticipate inflation to encourage them to spend more money now. Also, by spreading the belief that prices will start rising in a fast pace, the Fed can effectively reduce inflation-adjusted interest rates while stimulating the economy.

According to Dan Greenhaus of Miller Tabak & Co, "The Fed is on the verse of actively targeting a higher inflation rate." This practice is untested. It can potentially backfire if the inflation drifts further than the desired rate. In addition, it's not clear at this point whether expectations related to inflation can drive real and sustainable growth.

If you are interested in knowing more on the market signals we analyze, we encourage you tosubscribeto our Premium Updates to read the latest trading suggestions. We also have afree mailing list- if you sing up today, you'll get 7 days of full access to our website absolutely free. In other words, there's no risk, and you can unsubscribe anytime.

Thank you for reading.

Rosanne Lim

Sunshine Profits Contributing Author